Giving in retirement

Giving in retirement requires A LOT of faith. No more paychecks. Fewer career opportunities ahead. It’s just you and your investments. Uncertainty is now your certainty. And what’s the natural thing to do now that you are completely reliant on something out of your control? GIVE IT AWAY!!!

Of course, giving away your money is the opposite of what we’re inclined to do—our nature is to hoard rather than share. That’s why I admire those who step outside that instinct and open their hands in generosity.

With a high-five in admiration of your faith and generosity, let’s dive into three ways you can save on taxes and give even more to charity – a win-win.

First up: gifting stock directly to charity (also known as gifting appreciated securities).

Thanks for reading! Subscribe to receive weekly posts!

Gifting appreciated securities

- Do you have stocks in a non-retirement account (i.e., brokerage account)?

- Have they grown in value since you bought them?

- Have you held them for longer than a year?

If so, don’t sell them – give them directly to charity! Why?

Here are three reasons why:

- You avoid capital gains tax.

- The charity avoids capital gains tax.

- You get to deduct a larger amount (assuming you itemize).

That’s right! By giving the stock directly to charity – rather than selling it – you avoid capital gains tax. If you’re in the max capital gains bracket, that’s a 23.8% savings!

And even better, since charities don’t pay tax, they avoid the tax as well. This means no one pays the tax.

To top it all off, you can deduct the full market value of the security—not the amount you originally paid for it.

We call this a triple tax benefit.

Here’s an example to illustrate.

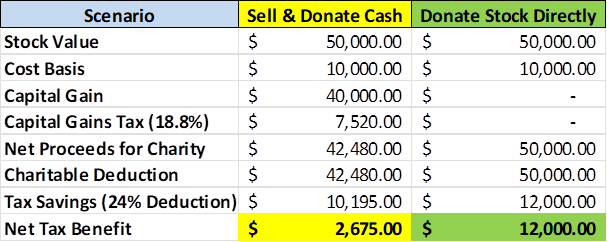

Robert, a retired executive, owns stock in a taxable account that he purchased years ago for $10,000. Today, that stock is worth $50,000. Wanting to support his church’s building fund, Robert considers selling the stock and donating the cash. However, selling would trigger $7,520 in capital gains tax, leaving only $42,480 to donate (assuming he’s in the 18.8% capital gains bracket). With this option, Robert would deduct $42,480, creating $2,675 in tax savings (at the 24% bracket).

Instead, Robert donates the stock directly to the church.

By doing so, he avoids the $7,520 capital gains tax entirely, claims a full $50,000 charitable deduction creating $12,000 in tax savings (24% bracket), and ensures the church receives the entire $50,000 tax-free.

Giving directly to charity rather than selling his stock creates an additional $9,325 in tax savings.

This approach lets Robert amplify his generosity while minimizing taxes – a win for both Robert and the church.

A no-brainer

If you’re a charitable retiree with a brokerage account, giving stock directly to charity is a no-brainer. Don’t sell that stock, give it directly to charity!

By giving directly, you can give more AND lower your tax bill.

In next week’s post we’ll explore a twist on this concept using a Donor Advised Fund (DAF). In the meantime, please reach out with any questions you have!

Disclosure: All written content on this site is for information purposes only. Opinions expressed herein are solely those of Ridley Wealth Management, LLC and our editorial staff. Material presented is believed to be from reliable sources; however, we make no representations as to its accuracy or completeness. All information and ideas should be discussed in detail with your individual adviser prior to implementation. Advisory services are offered by Ridley Wealth Management, LLC. Being registered as a registered investment adviser does not imply a certain level of skill or training.

The presence of this web site shall in no way be construed or interpreted as a solicitation to sell or offer to sell investment advisory services to any residents of any State other than the State of Texas or where otherwise legally permitted. All written content is for information purposes only. It is not intended to provide any tax or legal advice or provide the basis for any financial decisions. All investing involves risk including loss of principal. Past performance does not guarantee future results.

Ridley Wealth Management, LLC is not affiliated with or endorsed by the Social Security Administration or any government agency.

Images and photographs are included for the sole purpose of visually enhancing the website. None of them are photographs of current or former Clients. They should not be construed as an endorsement or testimonial from any of the persons in the photograph.